Locked Into a Low Mortgage Rate in the South Sound?

How to Know If Renovating Actually Makes Sense—Before You Spend a Dollar on Design

You bought your house when rates were in the low 3’s. Maybe you refinanced once or twice when the rates were tumbling.* You’ve gotten used to the manageable payments. The school is a good fit and the neighborhood is friendly.

But as you’ve grown into the house, have you grown out of it?

The kitchen was designed for a single person whose idea of cooking is making toast. The master bath has the most useless double sink vanity. You need a home office that isn’t the dining table. You’ve thought about an addition, maybe tearing out the back wall and starting over.

You’ve also thought about moving. Then you did the math.

A $500,000 mortgage at 3% costs about $2,100 a month. The same loan at today’s rates costs over $3,300. That’s a $1,200 monthly upcharge for the privilege of having a different house. It doesn’t get you a better house, just a different address.

“Millions of homeowners remain locked into mortgages with historically low rates, which means they are still inclined to stay put and improve their existing spaces.”

So…you stay. And you start thinking about what it would take to make this house work.

This is the right instinct. But it’s also where most homeowners open themselves up to expensive mistakes. Not for choosing wrong, but for starting in the wrong order.

* (I’m jealous. I’ve been dating an ugly rate for a long time now.)

Does it Still Make Sense to Stay and Renovate?

Before we get into renovations, additions, or design, let’s look at the financial picture. I asked Megan Higgs, a Gig Harbor mortgage professional with Canopy Mortgage, to walk through the numbers.

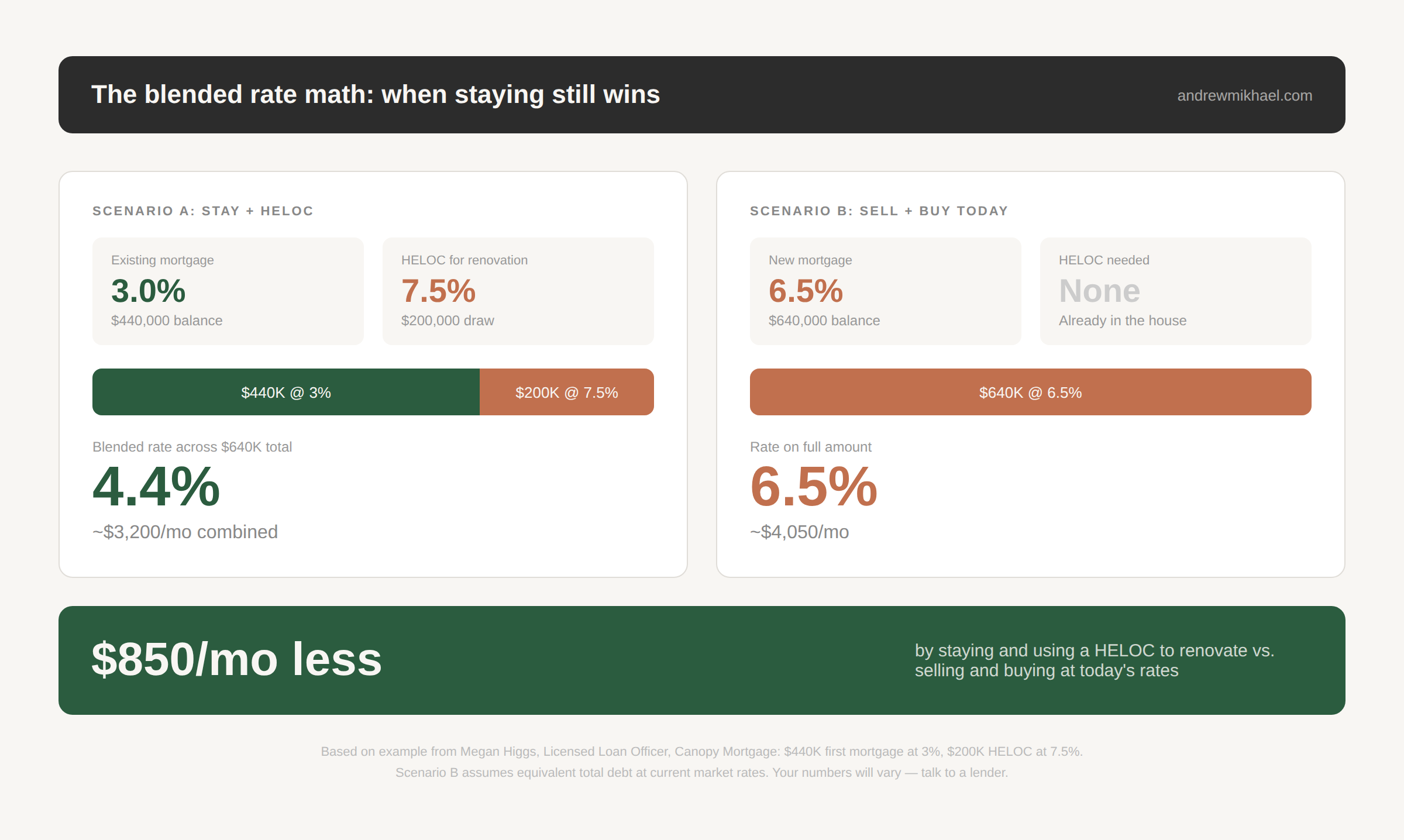

For most homeowners sitting on a 2 to 3 percent mortgage, the math still strongly favors staying in place and keeping that first loan intact. A homeowner with a $440,000 loan at 3 percent pulling $200,000 through a HELOC, even with rates in the 7 to 8 percent range, often ends up with a blended rate in the mid 4s. That is a meaningful gap compared to what that same homeowner would face if they sold, bought again, and financed the full purchase at today’s rates.

— Megan Higgs, Licensed Loan Officer

Blending a mortgage and HELOC to give you a real world monthly cost savings vs buying a new house.

Even borrowing $200K at a 7-something HELOC rate, you’re blending into the mid-4s. Still way better than selling and buying at 6.5%.

Lacie Ferris, a Fox Island Realtor, confirms this is reshaping how she advises clients:

This is probably the most important conversation I have with move-up clients right now. I’m very direct about it: if someone locked in at 3% or 3.5%, moving up means not just a larger mortgage, but potentially doubling their rate. So, I pull a lender in and we actually run the real numbers before we list their home. For some clients, the math still works because their equity position is strong or their income has grown significantly. But for others, that conversation is the reason they decide to renovate instead.

— Lacie Ferris, Fox Island Realtor

Lacie says this comes up in roughly a third of her listing conversations over the past 18 months. Sometimes the smartest move is walking away from a listing and telling someone to stay put.

I’m not in the business of talking people into selling. I’m in the business of helping them make the right decision for their family. Sometimes that means I walk away from a listing. But those clients remember that, and they send referrals because of it.

— Lacie Ferris

Megan draws the line at a specific threshold:

Where it starts to shift is when that blended rate gets within about 1 percent of current market rates, or when the renovation budget becomes large enough that the numbers start to compress. The decision really comes down to behavior, not just rate. A HELOC works best when the goal is to improve a home that already fits. Moving becomes the better option when the renovation starts to feel like a workaround instead of a solution.

— Megan Higgs

If you’re renovating because the house genuinely works for your life and you need to update it, the numbers are on your side. If you’re trying to force a house to be something it fundamentally isn’t, you might be better off moving and eating the rate hit.

Knowing which side of that line you’re on is the first question to answer. Not “what should my kitchen look like.”

“74% of outstanding single family home mortgages in Washington State are under 3%.”

How Do You Fund a Renovation Without Refinancing?

Most homeowners in this situation start Googling or asking AI about HELOCs. Reasonable instinct. But the options are more layered than most people realize.

Just because someone has $300,000 in equity does not mean all of it is safely usable. We still have to look at combined loan-to-value, payment comfort, credit profile, income, and whether the renovation budget is truly defined. The right solution is not just about access to cash. It is about how flexible the payment needs to be, how long they expect to carry that balance, and whether the renovation is cosmetic, structural, or something in between.

— Megan Higgs

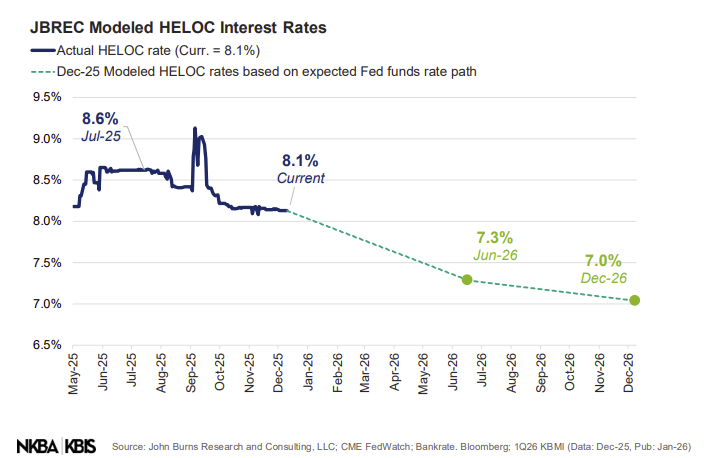

HELOC rates in the South Sound are hovering around the low 7s right now, tied to prime plus a margin. One thing Megan flags that most homeowners don’t think about: what happens after the draw period when you’ve been making interest-only payments, just like a new construction loan. That payment jump is where it gets real.

I’ve read the latest reports on the remodeling market nationwide and found that the HELOC rate is expected to go down to 7% by the end of the year, which means more borrowing power, and in turn more competition for the best designers and builders to undertake those renovations.

Researchers expect HELOC rates to decline towards 7% by December 2026

There’s also a tool most people don’t know exists: renovation loans. An FHA 203(k) lets you finance the renovation into the mortgage. It’s more structured than a HELOC, but for bigger projects it can be the cleaner long-term answer. Fannie Mae’s HomeStyle Renovation loan does the same on the conventional side.

FHA loans can be a pain. The escrow draws, the inspections, the paperwork. The hoops you have to jump through could seriously reduce the pool of architects and general contractors who are willing to deal with all that. It is a much heavier lift than a HELOC for everyone involved. But hey, knowledge is power.

Either way, if you’re not paying cash for a renovation, the financing conversation should happen before the design conversation. I’ve seen homeowners spend months developing a plan only to discover they can’t fund it. No one likes being in that spot.

Take The Move vs Improve Quiz

-

Take The Move vs Improve Quiz -

What Does A Renovation Actually Cost in Pierce County?

This is the section that will either confirm your gut or recalibrate it. I asked Kyle Bridgan of NSS Home in Tacoma to share real numbers from recent local projects.

Additions

Additions in Pierce County typically run between $350 and $1,000 per square foot, finished—not a shell. The range depends on the level of finishes, whether you’re adding mechanical systems or plumbing, and the installation codes and energy requirements that apply to your project.

— Kyle Bridgan, NSS Home

A 400-square-foot addition at $500 per square foot is $200,000. (Who said architects aren’t good at math?) That’s before permits, design fees, or site work. For a waterfront lot with shoreline setbacks and critical area buffers, you’re at the higher end of that range plus additional permitting and environmental review.

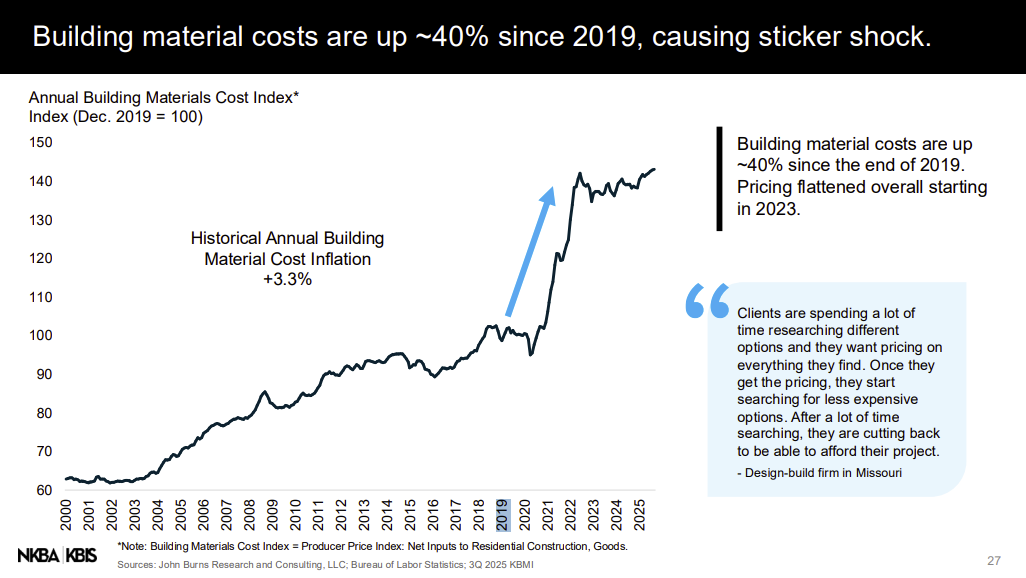

Building material costs are up 40% since 2019.

But an addition isn’t always the answer. I had a project in University Place where the homeowners were sure they needed one. The house had good bones but the layout was working against them. We looked at what was already there and found they could get everything they wanted, and more, by renovating the first floor. The biggest problem was that the kitchen was designed with 1960’s values (a utilitarian space tucked away). The clients otherwise loved the home and the location, but wanted the kitchen to be a more social part of the home. I found a way to reconfigure the layout to make that happen without feeling like a big exposed open plan from hell. We expanded the kitchen to become the center of the house with 360-degree views of the Puget Sound. Changed the roofline to gain height and a skylight. Redesigned the powder room in place. All under $300K on a house that’s probably worth over a million today.

The client told me it changed the way they talk to one another.

An addition would have pushed them further apart. The space they needed was already there. It just wasn’t being used right.

Numbers aren’t the only story. A big transformation is sometimes possible without a massive addition. That’s worth testing before you assume you need to build out.

Kitchen Remodels

Pricing a kitchen remodel is like pricing a car by the pound—too many variables for one clean number. And the age of your home changes the conversation entirely. An older home is like restoring a classic car—you came in for a paint job but once you pop the hood you’re replacing the engine, the transmission, and the wiring harness. That’s where most medium kitchens land between $120,000 and $160,000. A newer home is more like upgrading a late-model—the bones are solid, you’re swapping parts for better ones. A bare-bones pull-and-replace kitchen starts at around $75,000.

— Kyle Bridgan

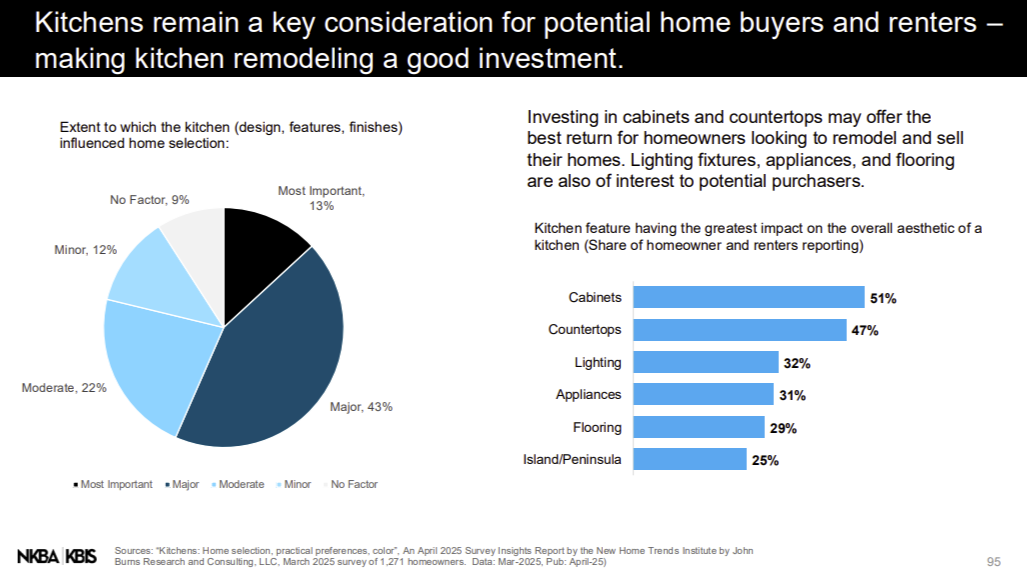

See the key features reported to have the greatest impact on a kitchen.

A lot of people come in thinking $30,000. Even an IKEA kitchen cabinet-only package can run $10k. Kyle says it can be done for less, but you’re sacrificing something to make that happen. You’re not to blame for having what those in the business might call an irrational budget. Kitchens are the most expensive room in a home pound for pound, even when not pricing by the pound.

Whole-House Renovations

These are case-by-case. Kyle’s team recently completed a 2,000-square-foot whole-home renovation for $784,000 and the majority of a 7,000-square-foot home for $287,000. The difference comes down to how many bathrooms you’re touching, how many rooms have specialty finishes, and what you find when you open up the walls.

Most clients focus their budget on one to three key rooms and do lighter cosmetic updates throughout the rest. The cost-per-square-foot metric doesn't apply the same way here. What I've always found with renovations is there's a slippery slope. Not just the "well we've come this far, why not go further?" mentality, but the quieter version: you replace the floors and now the trim looks wrong. You move a wall and now the flooring doesn't match. One decision creates three more, and each one has a price tag. Wait till you see how fast a nice wood floor's square foot price adds up.

The Costs Nobody Warns You About

Kyle breaks hidden cost drivers into two categories.

Older homes (pre-1950) hit you with what’s behind the walls. Framing issues, outdated mechanicals, aluminum wiring, asbestos, hidden knob-and-tube. Foundation settling. Everything renovation-related costs more in a house built before 1950.

Newer homes (post-1980s) surprise people with construction defects from newer materials.

In remodeling in general, Kyle sees homeowners assume something is part of the scope when it was never in the original agreement. Homeowners assume something is part of the price when it was never in the original scope. That gap is where budgets unravel.

In Gig Harbor and Fox Island, waterfront properties add another layer entirely. Shoreline regulations, septic systems, steep slopes, and critical area buffers can all limit what’s possible before you even talk about design. I write about this a lot because it catches people off guard. Megan sees the same thing from the lending side:

In Gig Harbor, financing a renovation is not just about equity and rate. It is also about the property itself. Waterfront homes, older homes, septic systems, topography, and shoreline regulations can all affect cost, permitting, and timeline. Two homeowners with the same amount of equity can have very different renovation paths depending on where the property sits and what they are trying to do.

— Megan Higgs

This is why I run feasibility before design. Two houses across the street from each other can have completely different zoning constraints, buildable areas, and permit paths. If you don’t know that before you start drawing, you’re guessing with serious money and substantially different project timelines.

When Does Renovating Stop Making Sense?

Lacie puts a number on it:

My general rule of thumb: once you’re looking at $150,000–$200,000+ in renovations, especially if the project requires temporary displacement, that’s when the conversation gets serious. At that budget, you’re often better off channeling that money into a move, particularly if the renovation still won’t give you everything on your wish list. The exception is when someone has a truly irreplaceable lot, location, or view.

— Lacie Ferris, Fox Island Realtor

That exception is important in the South Sound.

A waterfront lot on Fox Island or a view lot overlooking Henderson Bay is not something you replicate by moving. If the property is irreplaceable, if you love more than you hate about the home and the neighborhood, the renovation math changes. If it’s just a house, $200K in renovations might be the wrong play.

I’d add one thing to Lacie’s framework. Budget alone isn’t the deciding factor. It’s what the budget gets you. The University Place project I mentioned was under $300K, but it completely changed how that family lives in their home. A $300K addition on the wrong house might not accomplish half as much.

The question isn’t just “how much” but “how much of the problem does this actually solve.”

Will You Get Your Money Back?

Lacie’s honest answer:

Full renovation ROI in Pierce County is still pretty mixed. Kitchens and bathrooms remain the strongest performers—clients are generally recouping 60–75% of those costs at resale, sometimes more if the finishes hit the right price point for the neighborhood. Large additions are trickier. I’ve seen significant square footage additions where the appraised value didn’t come close to covering the build cost, especially in neighborhoods where the comps just don’t support a higher price.

— Lacie Ferris

You rarely get dollar-for-dollar back on major projects. The best returns happen when the renovation brings the home up to the standard of the neighborhood rather than beyond it.

Paige Schulte, Realtor and founder of Neighborhood Experts, frames the other side of that equation. She calls the discount buyers apply to un-renovated homes a “pain tax”:

In the current market the homes that are appreciating quickly and for the most money are ones that are 100% turn-key.

The difference in price is quite impressive. Buyers understand the cost of a remodel and the time it takes. Along with the cost to update they do not want to slog through the update. We call it a pain tax off the price.

— Paige Schulte, Gig Harbor Realtor

Buyers discount homes that need work by more than the work would actually cost. They’re pricing in the hassle, not just the dollars. So even at 60–75% ROI on the renovation itself, you may be avoiding a larger loss by not selling the house un-renovated.

In my experience as an architect, custom home clients, and in turn renovation clients, are those who 1. Look at the market and say none of this suits me, 2. Have the patience, and 3. The budget to make something that does.

So either way, it’s worth knowing and owning who you are.

The Two Most Expensive Mistakes

Kyle sees it from the construction side:

Not bringing a contractor in early enough. Homeowners go through the entire design process, fall in love with a plan, and then bring it to a contractor only to find out it’s over budget or just unnecessarily complicated. Now you’re redesigning, cutting things out, and settling for less than what you could have had if the contractor had been at the table from the beginning.

— Kyle Bridgan

Lacie sees the same pattern from the real estate side:

Without question: scope creep and emotional attachment to a number. Homeowners will come in with a $100K budget and a clear plan, and six months later they’re at $220K because one decision led to another. The other blind spot is not accounting for the disruption cost—living through a major renovation is genuinely hard, and that stress has real value that people underestimate when they’re doing the math.

— Lacie Ferris

I’ll add a third one I see constantly: assuming you need an addition when you don’t. Most homeowners jump to “we need more space” when the real problem is how the existing space is organized. A good feasibility study tests that assumption before you’re committed to a $200K+ addition that might not have been necessary.

The fix for all three is the same. Get a builder, an architect, and a realistic budget aligned at the same time. Not one after another.

What the Move-Up Market Actually Looks Like

If you’re still considering moving instead of renovating, here’s what the $800K–$1.5M market looks like right now in the South Sound:

Inventory in the $800K–$1.5M range is still tight, but for different reasons than a year or two ago. Buyers at that price point are finding “something,” but finding exactly what they want is a different story. Well-maintained homes with updated kitchens, good lot size, and a view or waterfront element are still moving quickly. The inventory that IS sitting either has a layout issue, deferred maintenance, or a price that doesn’t reflect the current market reality.

— Lacie Ferris, Fox Island Realtor

So even if you decide to move, the house you want may not exist. And if it does, it’s already updated and priced accordingly. You’d be paying someone else’s renovation premium plus a higher mortgage rate.

Renovate Smart, Not Weird

Paige Schulte shared something worth hearing. I asked her about renovations that actually hurt resale:

The biggest ones are just missed opportunities. A kitchen remodel that didn’t improve a view, or a wall that was put up and reduced lighting. A bathroom remodel that shrunk the closet. Or a new build that doesn’t account for functionality of how a home actually lives, vs what looks sexy.

— Paige Schulte, Real Estate Agent

Every one of those is a fundamental design problem, not a construction problem. A contractor builds what the plans say. The question is whether the plans are solving the right problem. This is what I spend most of my time on. Not picking finishes. Figuring out what the house needs to do differently, and testing whether that’s actually possible on the site, within the zoning, and inside the budget.

You ever walk into a home and said, “What were they thinking?” Let’s avoid that, shall we?

How Long This All Takes

Lead times on products have stabilized. Upscale windows and cabinets are running 6 to 8 weeks from most suppliers. Contractor schedules in the South Sound are booked about a quarter out for major renovation design work.

Kyle makes a point worth repeating:

The real driver of any project schedule is how fast the homeowner can make up their mind and get design decisions finalized. That’s the bottleneck more than contractor availability. And here’s a tip: if a contractor can start right away, that’s a red flag. Do you want the brain surgeon who can see you right away or the one you have to schedule out?

— Kyle Bridgan

I’ll add, there’s a rookie mistake people make thinking they can design on the fly and pick out finishes as they go. The idea is usually to rush to permitting to speed the process. The result is always the same. They get derailed with the options, the contractor sends the installers out to another job and they don’t come back when your products are delivered, they come back when they’re done with whatever jobs they went to that were better organized. I won’t work that way.

Should You Wait for Prices to Drop?

No.

Material costs have stabilized—but they’ve stabilized at a high level. There are tariffs on the horizon, but luckily, we don’t dabble with a lot of imported goods on most of our projects, so we’re not seeing anything like the COVID days. What we are seeing is that the big manufacturers have gotten smart about issuing periodic price increases to create urgency. My advice for anyone planning a 2026–2027 project: don’t wait expecting prices to come down. Budget for where things are now and build in a cushion.

— Kyle Bridgan, NSS Home

Waiting for materials to get cheaper is the renovation version of timing the stock market. You’re more likely to lose months of living in a house that doesn’t work than you are to save 5% on cabinets.

This one’s Italian, if you’re keeping score.

Maybe it’s my love of Italian and German plumbing fixtures muddying the waters, but I’ve heard rumors in the industry of some US brands raising prices to match tariffed rates.

I don’t like either side of that, but I say it to say, get what you want.

Where to Actually Start

If you’re reading this, you’re probably somewhere between “this house isn’t working” and “I have no idea what this will cost or if it’s even possible.”

Before you hire an architect, before you call a contractor, before you start pulling up kitchen inspiration on Pinterest, there are three things to figure out:

1. What does your property actually allow? Zoning, setbacks, lot coverage, height limits, shoreline buffers, septic capacity. In Pierce County, these aren’t minor details. They define what you can and can’t do. I’ve seen homeowners spend $15,000 on design for additions that couldn’t be permitted.

2. What does the financing picture look like? Talk to a lender before you talk to a designer. Know your realistic budget, not your aspirational one. Megan’s point about combined loan-to-value and payment comfort is something most people don’t think about until it’s too late. You don’t have to know what any particular design might cost, but you ought to know what YOU are willing to spend.

3. Is the renovation solving the right problem? This is the one most people skip. Lacie’s $150K–$200K threshold is a useful gut check. But so is the University Place question: do you actually need more space, or do you need your existing space to work differently? Those are two very different projects at two very different price points.

This is what I do in a Site Validation. It’s a feasibility study that answers these questions before you commit to a direction. Zoning, structural constraints, permitting realities, realistic cost ranges, and whether the house can actually give you what you need. It takes a few weeks. It costs a fraction of what a wrong decision costs.

If you’re sitting on a low rate in the South Sound and wondering whether renovating makes sense, start there. Not with a floor plan. With clarity.

CONTRIBUTORS

Megan Higgs — Loan Officer, Canopy Mortgage

Lacie Ferris — Fox Island Realtor

Kyle Bridgan — General Contractor, NSS Home

Paige Schulte — Gig Harbor Realtor, Schulte & Co Team, Neighborhood Experts

Thinking about a renovation or addition in the South Sound?

A Site Validation helps you understand what’s possible on your property, what it will realistically cost, and whether the project makes sense before you invest in design. Start with clarity, not a floor plan.

Thank you to Lacie, Megan, Paige, and Kyle for your contributions to this article!

Andrew Mikhael is an architect in Pierce County and the President of the National Kitchen and Bath Association’s Olympic West Sound Chapter.